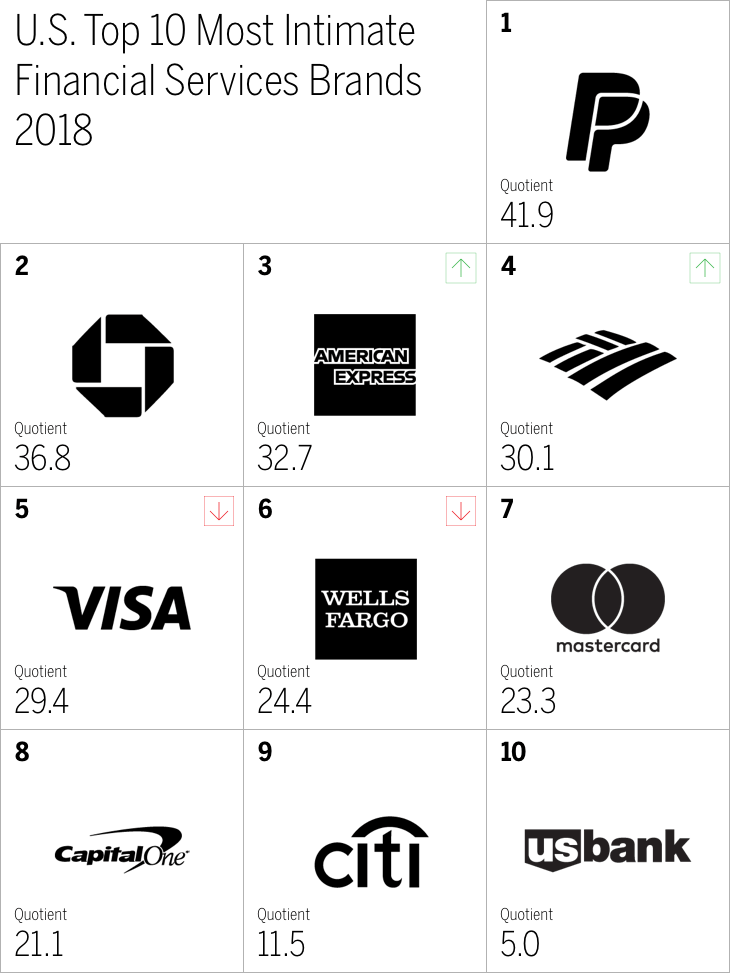

Overview

- Between 2017 and 2018, the financial services industry has dropped from #6 out of 15 to #10

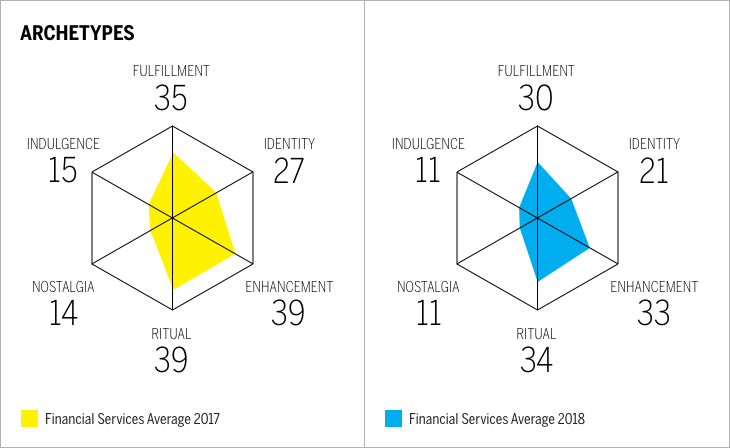

- Both the enhancement and identity archetypes have dropped six points over the last year

- Millennials have lower levels of Brand Intimacy with financial services brands than the average user (19.5 vs. 22.9)

- The percentage of customers in the most advanced stage of Brand Intimacy (fusing) has dropped significantly since 2017, from 5 percent to 2 percent

Consumers can have complicated relationships with financial services brands. Banks, credit cards, and digital payment platforms empower us to do more with our money, but they can also be associated with all of the responsibility, stress, and anxiety that comes with managing and planning our financial lives.

This year, it seems consumer sentiments toward the financial services industry have taken a turn for the worse. Of the 15 industries in our annual Brand Intimacy Study, financial services has dropped from #6 in 2017 to #10 in 2018. This drop in overall performance as well as in nearly all of our Brand Intimacy metrics signals a falling out between consumers and the brands in this industry, so we thought we’d use our data and understanding of the category to make some key observations and insights into how marketers in financial services can build stronger, more intimate relationships with their customers.

1. Keeping up with technology isn’t enough

Financial services brands have been implementing new technology-enabled features over the years, from mobile banking apps to biometric security and chatbots. This is partly the result of fin-tech brands and industry disruptors entering the market and acting as forces for innovation. Although new features help deliver information, convenience, and peace of mind, our data reveals that they don’t resonate with consumers. Looking at the financial services industry through the lens of enhancement (the Brand Intimacy archetype most associated with technology that characterizes a brand as making the user smarter, better, and more connected), we see a significant decline in performance.

Brand Intimacy archetypes: 2017 vs. 2018

With a six-point drop in the enhancement archetype, it’s clear that consumers are feeling less connected to financial services brands than they used to. Banks and credit card companies continue to roll out new technology-enabled features, but consumers aren’t forming stronger bonds with their banking brands. Technology features have become table stakes, with each new one quickly being copied and becoming standard among most brands.

The key takeaway: Although keeping up with technology trends is basic, it isn’t enough to motivate consumers. Brands need to enhance the emotional connection through essence, story, and experience in ways that set them apart.

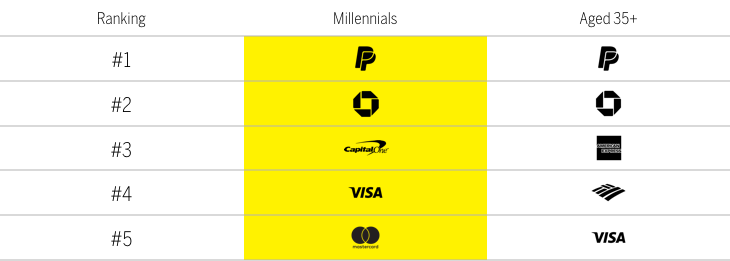

2. Millennials are saying “meh”

It may not come as a surprise that millennials aren’t as close with financial services brands as older generations—being a bank member or credit card holder these days isn’t as much as a commitment as it used to be. In our study, millennials have lower levels of Brand Intimacy with the financial services industry compared to users over 35 (19.5 vs. 22.9).

Top 5 financial services brands by age group

What’s more troubling for marketers trying to connect with younger consumers is the drop in millennial intimacy since last year. In 2017, financial services was the #8 industry for millennials, with an average Brand Intimacy Quotient of 28.8. This year, the industry has dropped to the #12 spot for this demographic with an average Brand Intimacy Quotient of 19.5. These low levels of Brand Intimacy for financial services brands is reflected in millennials’ behavior: they have lower levels of customer engagement with their primary banks than baby boomers (30 percent vs. 40 percent). Millennials are also 2.5 times more likely to switch their primary bank than baby boomers and 1.5 times more likely than Gen Xers. But indifference from millennials also means there are opportunities to capitalize on shifting attitudes. For example, if financial services brands can offer services and features that empower or reward the cashless lifestyle, millennials are likely to respond favorably because they are 41 percent more likely than any other generation to see paying in cash as inconvenient.

The key takeaway: When it comes to financial services, millennials are less intimate, less engaged, and more likely to switch banks than older generations. If brands hope to build loyalty with younger audiences, they need to adapt to shifting attitudes and behaviors and embrace a cashless future.

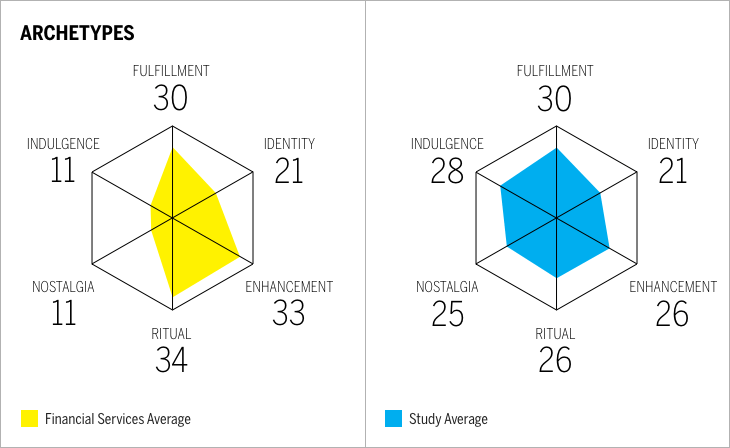

3. Identity is on the decline

The identity archetype describes attributes that reflect an aspirational image or admired values that resonate deeply. American Express leads in this archetype in financial services. Like enhancement, the identity archetype dropped six points in the industry since last year. Financial services brands (especially credit cards and banks) have been strongly associated with identity, built on ideas such as trust, security, status, and financial responsibility. It’s both surprising and telling that the industry’s identity score is roughly the same as the cross-study average (21).

Brand Intimacy archetypes: financial services vs. study average

Of the six Brand Intimacy archetypes, identity is only the fourth-strongest in the category, ahead of nostalgia and indulgence. In an industry in which several brands are offering similar products and services, the lack of differentiation and the attributes captured through the identity archetype signals that these brands are increasingly becoming commoditized. For example, a 2016 survey found that the types of rewards a credit card offered was nearly twice as important to the attractiveness of the card as its brand. Consumers can easily compare costs and features across competitors, and although this might signal trouble for the industry, it’s a strong indication that practical benefits are becoming more important to the decision-making process. Another factor affecting identity scores could be consumers’ distrust of financial institutions in the wake of the Great Recession and events like the Wells Fargo scandal. This erosion of trust can negatively impact loyalty and make it difficult for consumers to identify with the a brand.

The key takeaway: Identity is an important part of how consumers connect with brands, especially in financial services, where status, trust, and security are essential. Although the role of identify is not lost and brands will need to rebuild consumers’ trust and respect going forward, in the meantime, they should recognize that people are more likely to respond to practical benefits, such as rewards, low interest rates, and payment flexibility.

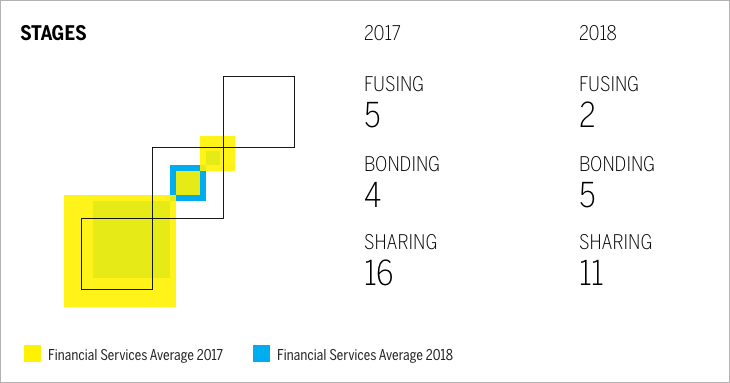

4. Fewer die-hard fans

Overall, consumers aren’t connecting as strongly with financial services brands as they were last year. It’s clear that Brand Intimacy is on the decline in this industry, but it’s also worth noting that this drop in intimacy is most severe among the strongest consumer–brand relationships. The three stages of Brand Intimacy identify the depth and degree of intensity in these relationships, from the least advanced stage, sharing, to the most advanced, fusing. The more intimate consumer are with a brand, the more they are willing to spend and the less they are willing to live without that brand.

Stages of Brand Intimacy: 2017 vs. 2018

The fusing stage is when a person and brand are inexorably linked and their identities begin to merge. Since last year, the percentage of users in this stage has dropped by more than half, from 5 percent to 2 percent. The second-most advanced stage, bonding, saw a slight increase of 1 percent (perhaps taking on some users that were formerly in the fusing stage), and the percentage of users in the sharing stage fell from 16 percent to 11 percent. This might be our most concerning observation about the industry. Fewer users in the fusing stage signals indifference toward financial services brands. However, the general shift toward indifference within the industry also means that marketers have an opportunity to make their brands stand out. If they can appropriately respond to today’s shifting attitudes, they can start to find new ways to connect emotionally with consumers, thus differentiating themselves within the category.

The key takeaway: Fewer users in the most advanced stage of Brand Intimacy indicates that consumers are less willing to form close relationships with brands in this category. This significant drop in fusing consumers is likely related to the other trends affecting Brand Intimacy in this industry. As our concept of “money” continues to transform with technology, so too will consumer relationships with financial services brands, making yesterday’s marketing approaches insufficient and obsolete. If marketers in this industry are able to respond to current trends, they can rebuild the emotional bonds between their brands and their customers and identify ways to build entirely new bonds as well.

As the landscape of financial services changes, brands face new challenges for creating and maintaining intimate bonds with consumers. To counteract the industry’s current shift toward indifference, banks, payment platforms, and credit card providers should be incorporating differentiated technology features, adapting to millennial attitudes and behaviors, and prioritizing practical benefits and services. By taking these steps (and others in the future), financial services brands can change the way consumers feel about them and work toward greater levels of Brand Intimacy.

Get an overview of Brand Intimacy here.

Read our detailed methodology here and review the sources cited in this article here. Our Amazon best-selling book is available at all your favorite booksellers. To learn more about our Agency, Lab, and Platform, visit mblm.com.