Retail is the third most intimate industry in our 2017 Brand Intimacy Study, following automotive and media & entertainment. This is a strong showing, although it ranked second in our previous study. This category contains a diverse array of brands ranging from specialty stores that sell food, beauty products, and home furnishings to generalists with broad department-store offerings. It is clear we rely on these brands for everyday living and appreciate them for the convenience they provide.

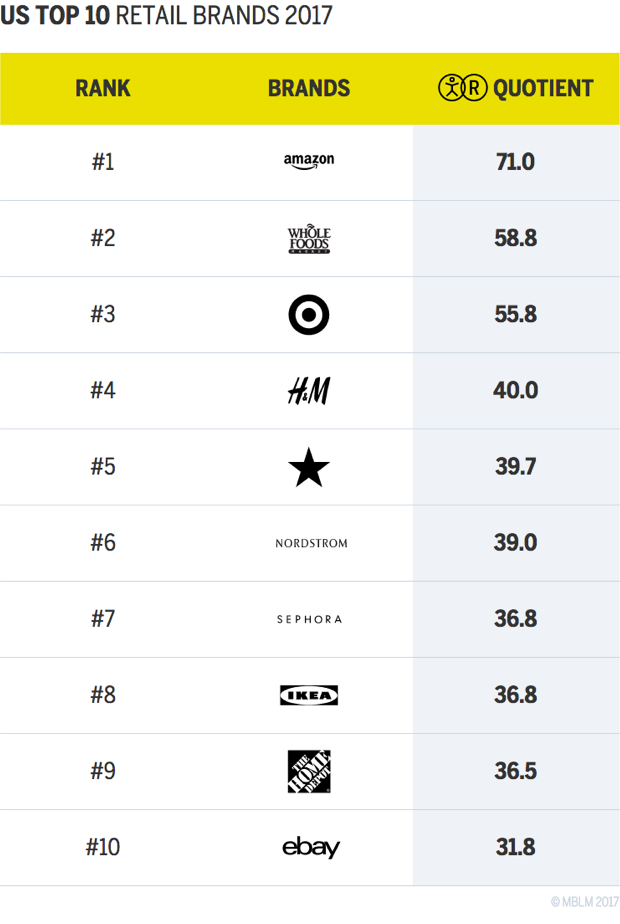

Online-retailing giant Amazon firmly leads our list of Top 10 Retail Brands, followed by Whole Foods. Target is our third brand in the category, overcoming Sephora since our previous study, along with H&M, Macy’s, and Nordstrom. Amazon has the largest percentage of customers in the fusing and sharing stages of intimacy (12 percent and 26 percent, respectively), while Target leads in the bonding stage with 14 percent.

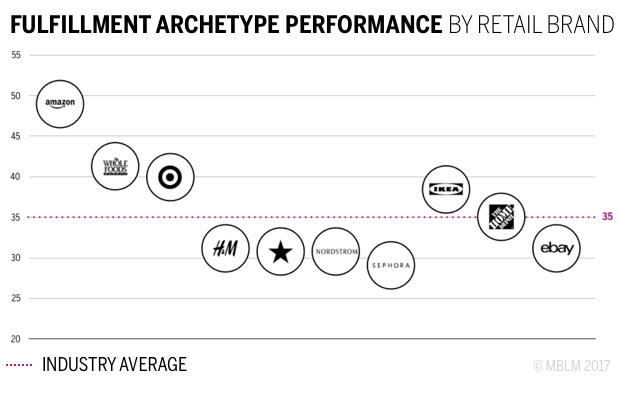

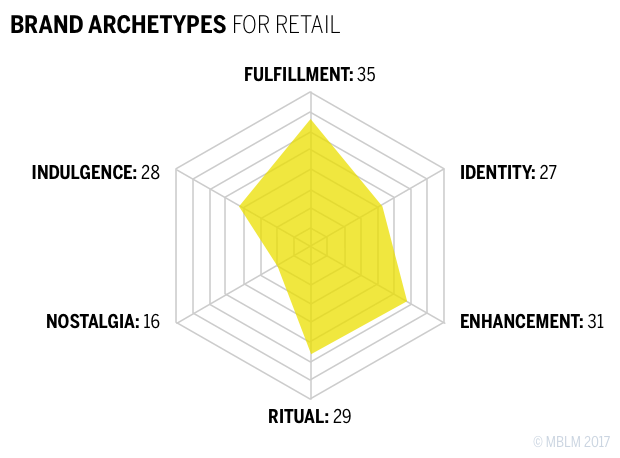

The retail industry is most associated with the fulfillment archetype, which relates to exceeding expectations and delivering superior service, quality, and efficacy. In the chart above, which shows the relationship between a brand’s fulfillment score and its brand intimacy ranking within the industry (from left to right), fulfillment is positively correlated with intimacy except among retailers H&M, Macy’s, Nordstrom, and Sephora. Interestingly, these brands make up for lower fulfillment scores with relatively high scores in the indulgence archetype, which is characterized by brand relationships centered on moments of pampering and gratification.

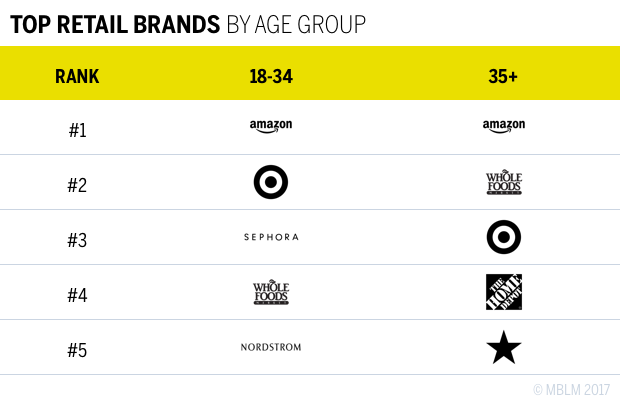

Examining the industry by age group, reveals considerable similarities between younger and older audiences. Consumers both under and over 35 rank Amazon as their number-one retail brand. Also, both groups rank Target and Whole Foods within their top five brands, with younger consumers preferring Target and older consumers favoring Whole Foods. On average, younger consumers are more intimate with retail brands, with an average brand intimacy quotient of 45.3 for the industry, compared with 41.3 for consumers over 35. Although both age groups rank Amazon first, millennials are significantly more intimate with the brand, averaging a quotient score of 75.2, compared with 68.6 for older consumers.

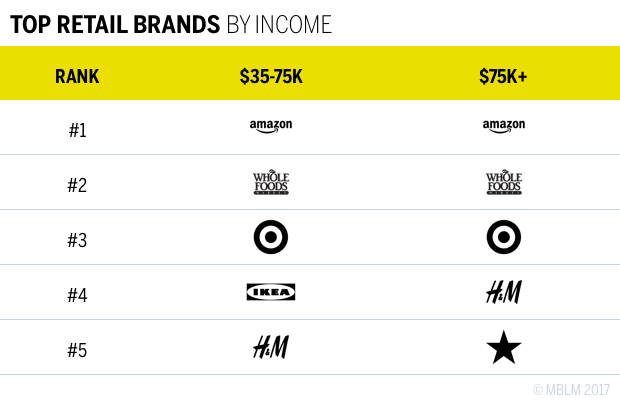

On average, higher-income consumers are more intimate with retail brands. Those earning over $75,000 have an average quotient score of 45.6, compared with 40.4 for those earning less than $75,000, but the two groups show similar brand preferences. Both higher- and lower-income consumers choose Amazon, Whole Foods, and Target as their number-one, number-two, and number-three retail brands, respectively. Also, H&M makes the top five for both groups, suggesting that income may not be a major factor in how consumers select retail brands.

Retail is one of only five industries that has more success building bonds with women than it does with men, along with consumer goods, fast food, health & hygiene, and apps & social platforms.

Although retail is our number-three industry overall, it is the leading industry among women, with an average brand intimacy quotient of 46.5, compared with only 37.7 among men. This discrepancy between men and women (8.8) is the largest for any industry in the study and could indicate an opportunity for brands in the category to appeal actively to men more strongly. Some retail brands have done this successfully, such as Amazon and Whole Foods, which are the fifth and ninth most intimate brands for men, respectively. Also, for the first time ever, men are currently outspending women by 13 percent in the retail category, and some predict that the menswear market will expand by 8.3 percent in 2017, which is more than 1.5 times more than what is predicted for the womenswear market.1 This could present an opportunity for clothing retailers to target men in the years to come.

The Amazing Amazon

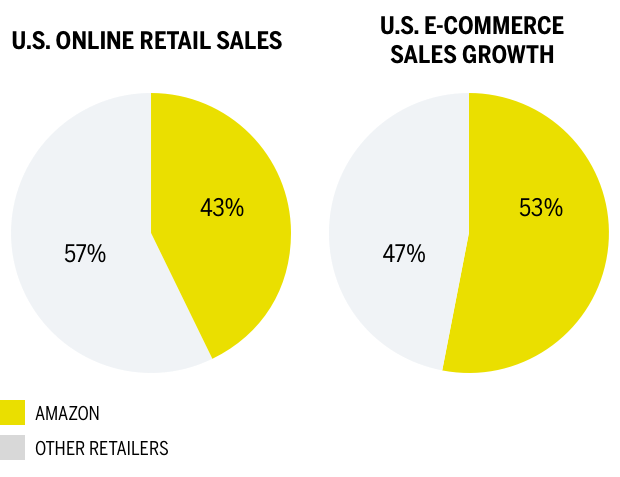

Of all the brands in this category, one truly stands out. In 2016, Amazon accounted for 43 percent of all online retail sales in the United States (up from 33 percent in 2015) and 53 percent of growth in e-commerce sales.2 In terms of brand intimacy, Amazon is the clear favorite of the category. It is the number-one retail brand for men and women, all income groups, and all age groups but one (45–64 year olds, who prefer Whole Foods).

In addition to dominating online retail, Amazon has an impressive suite of other businesses, some of which positively affect its e-commerce sales. For example, owners of Amazon’s smart speaker device, Echo, spend around 10 percent more on Amazon in the six months after they buy Echo, compared with the six months before.3 Amazon Prime members spend almost three times as much as non-Prime members do.4 Prime memberships offer e-commerce benefits (fast, free shipping on certain items) and media-streaming services (Prime Video, Prime Music, Prime Channels, Prime Reading, etc.), which more than doubled in consumer consumption in 2016.5 Amazon is leveraging its suite of products and services to drive e-commerce. CEO Jeff Bezos claims that his goal is to make it “irresponsible” not to be a Prime member, offering such appealing benefits to make the $99-per-year membership an obvious choice.6

Amazon goes to great lengths to please its customers and offer superior convenience. Recently, the company invested heavily in shipping to make delivery even faster by leasing planes from cargo companies, buying trucks, and building delivery drones.7 Amazon CFO Brian Olsavsky believes that these investments are necessary, saying, “We acknowledge that’s expensive, but it’s certainly a great part of our value proposition, and customers love it, so we take it as a given and then we work very hard to bring down our costs through greater efficiency.” This dedication to improving and giving customers what they want explains how Amazon scores so highly in the fulfillment archetype (sixth in the study): the brand continually strives to exceed customer expectations.

The Collapse Of Retail

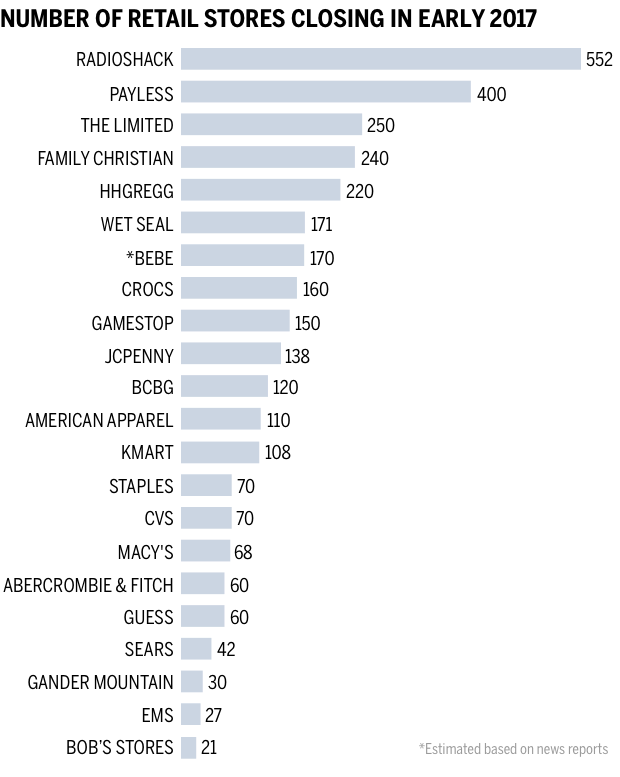

While retail brands perform well in terms of their abilities to create intimate relationships, it is clear that the dominating success of Amazon and the digitization of the industry have hit traditional retail brands hard. Macy’s, Sears, Kohl’s, J.C. Penney, and Dillard’s have collectively closed 700 stores since 2013, and Macy’s is planning to close another 100 in 2017.9 A list of store closures in early 2017 demonstrates the breadth and range of the collapse.10

Much of this is due to the capital investments that these retailers need to make in technology and omnichannel buildout to keep up, making it harder for them to grow and profit. Additionally, many feel experience in current retail stores is lacking, with stores dilapidated after years of underinvestment and/or staff being hard to find, leading to long lines at the register and/or few salespeople.

Some brands have responded positively and incorporated new technologies into their businesses. Sephora has embraced chatbots and now allows customers to book appointments for makeovers at it stores.11 EBay released ShopBot, a personalized shopping assistant that works through Facebook Messenger and helps customers shop for items and find gifts.12 Brands have also used technology to enhance the brick-and-mortar experience, such as H&M’s and Sport Chek’s launch of technology-enabled outlets that use minimal inventory and create environments that invite consumers to engage, interact, and be social.13

Because the retail industry primarily builds bonds through associations with fulfillment, consumers become intimate with the retailers that continue to deliver quality, improve service, and exceed expectations. Currently, Amazon is winning. Other brands in the category will need to carve out and defend their own spaces if they hope to avoid the fate of Macy’s and others.

Brand intimacy is key for a category floundering like this one is Brands must look to position themselves around emotion (not many do) and build relationships as a first step, embracing customers rather than seeing them as transactions. Campaigns, social media and advertising are important vehicles to promote more than discounts. Brands must nurture the brand–customer dynamic with communications and initiatives, not just through offering coupons—they can achieve this by acknowledging customers and what’s important to them today. Service, be it online or at retail, needs to become more focused on delivering the critical archetype of fulfillment and making the shopping experience positive and pleasant. Retail brands need to focus on delivering smarter, more convenient, more delightful ways to exceed customer expectations. Brick-and-mortar stores need to do more than replicate their online versions if they want to maintain them; they must provide extraordinary experiences. Relatedly, online stores must be best in class; there are simply too many competitors to offer a mediocre shopping destination. Intimacy tools that measure customer sentiment and communications built toward promoting engagement and designing retail experiences for the way people make decisions should be top priorities on any retailer’s list. Brands should look at what other archetypes they can leverage to help build intimate bonds and should be one step ahead of customer needs rather than miles behind.

Looking ahead, it’s hard to know how the industry will continue to transform. Can other brands compete in the digital space, or will they soon be using Amazon Go technology to power no-checkout shopping experiences, giving Amazon yet another massive revenue stream to feed its empire? In any case, even as retail becomes increasingly digital, it remains a highly consumer-centric industry built on convenience, quality, and experience. If retail brands can continue to offer competitively fulfilling consumer experiences, they can continue to thrive and remain a strong category for intimacy.

Get an overview of Brand Intimacy here.

Read our detailed methodology here and review the sources cited in this article here. Our Amazon best-selling book is available at all your favorite booksellers. To learn more about our Agency, Lab, and Platform, visit mblm.com.